Where Have Car Insurance Rates Decreased in 2026?

-

Jessica Richmond is a content writer and strategist with more than 12 years of professional experience creating content for digital and print audiences. Throughout her career, she has written for…

-

Rose Carter is an accomplished content strategist and marketing leader with a proven track record of creating impactful, results‑driven content. With expertise in writing, editing,…

-

- Senior Vice President, Business Intelligence & Analytics

- 26 years of industry experience

A results-driven leader, Hung Huynh is a seasoned expert in analytics, boasting a rich career spanning over 26 years across various business, operations …

Car insurance rates have climbed sharply across the country in recent years, putting extra pressure on drivers already dealing with higher vehicle prices, repair costs, medical expenses, and everyday inflation.

According to the Freeway Insurance 2026 Auto Insurance Rates Report, average auto insurance premiums increased approximately 23% nationwide from 2023 to 2026. More than 45 states experienced double-digit rate increases over that period, and 14 states saw increases of 30% or higher.

Some markets experienced even larger changes. New Jersey saw car insurance rates increase by 57%, followed by Washington at 51% and the District of Columbia at 50%. Want to see where drivers are facing the biggest increases? Read The 10 States Where Car Insurance Is Rising Fastest in 2026.

While long-term costs remain higher than they were a few years ago, Freeway Insurance data shows a more complex story. In some states, average car insurance premiums decreased from Q1 2025 to Q1 2026, signaling that certain markets may be experiencing signs of stabilization.

Using actual customer policy data, this analysis highlights the states where auto insurance rates decreased the most in 2026 and explores some of the market factors that may contribute to lower average premiums.

Unlike quote estimates or broad industry projections, this Freeway Insurance report analyzes real policies purchased by customers under actual underwriting conditions.

The findings below are based on single-policy, single-driver auto insurance policies, comparing Q1 2025 with Q1 2026. For more information about how the data was collected and analyzed, review the Data Methodology.

While some states experienced decreases in average premiums, that does not mean every driver saw their rate go down. Auto insurance is highly personalized and can vary based on factors such as location, driving history, vehicle type, coverage level, age, credit where allowed, state regulations, weather-related risks, accident trends, and other rating factors.

However, the data suggests that while affordability challenges remain, some insurance markets may be beginning to stabilize after several years of significant rate increases.

States Where Freeway Customers Saw the Biggest Auto Insurance Rate Decreases in 2026

The biggest decreases were not limited to one region. States across the South, Northeast, Midwest, West, and Pacific Northwest all saw average premiums move lower year over year.

*States are ranked by year-over-year percentage change in average premium for single-policy, single-driver auto insurance policies, comparing Q1 2025 with Q1 2026.

The biggest takeaway: rate relief was not limited to traditionally low-cost states. Florida, New York, Oregon, Arizona, Georgia, and Texas all face different insurance pressures, yet each saw average premiums move lower year over year in Freeway’s data. That suggests the 2026 insurance market is uneven, with some drivers seeing relief while others continue to face higher costs.

Average Monthly Premiums Before and After the Decrease

Drivers in many states are paying less for auto insurance than they were a year ago. The following chart compares the average monthly premium during the first quarter of 2025 with the average monthly premium during the first quarter of 2026, highlighting how rates have changed across ten states.

*This chart compares average monthly premiums for single-policy, single-driver auto insurance policies in Q1 2025 and Q1 2026. Data is based on actual Freeway Insurance customer policies.

Biggest Dollar Drops in Average Monthly Premium

Some states with similar percentage decreases produced very different dollar changes. Florida, New York, and Oregon had the largest monthly premium drops among the states analyzed, with average premiums falling by more than $30 per month.

*Monthly premium difference is calculated by subtracting the Q1 2026 average monthly premium from the Q1 2025 average monthly premium. Negative values indicate lower average premiums in 2026.

State-by-State Look at Where Auto Insurance Costs Decreased

Understanding local factors — including claim patterns, insurer competition, weather exposure, vehicle repair costs, traffic congestion, and policyholder mix — can help explain why drivers in some states may be seeing relief.

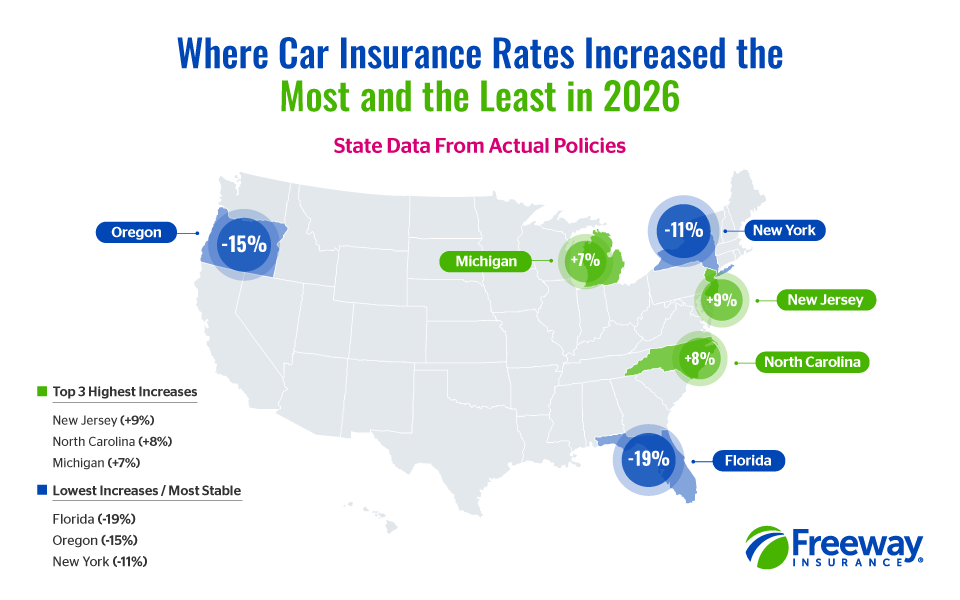

1. Florida: Average Rates Fell 19%

Florida had the largest decrease in Freeway’s data, with average premiums falling 19% from Q1 2025 to Q1 2026.

That decrease is especially notable because Florida has often been associated with high insurance costs due to severe weather risk, litigation, dense traffic, and expensive claims. A year-over-year drop does not mean Florida has suddenly become a low-cost state for car insurance, but it may suggest that some parts of the market are beginning to stabilize after years of pressure.

Still, Florida drivers should not assume rates are low across the board. Premiums can vary significantly by ZIP code, driving record, coverage level, and carrier.

Learn more about car insurance in Florida.

2. Oregon: Average Rates Fell 15%

Oregon saw the second-largest decrease, with average premiums falling 15% year over year.

Insurance costs in Oregon can be influenced by urban traffic patterns, weather-related claims, vehicle repair expenses, and regional carrier pricing. The decrease suggests some Freeway customers in the state may be seeing relief after prior market pressure.

Learn more about car insurance in Oregon.

3. New York: Average Rates Fell 11%

New York’s average premiums fell 11% from Q1 2025 to Q1 2026.

Even with that decrease, New York drivers may still face higher insurance costs than drivers in many other states. Dense traffic, medical costs, theft risk, no-fault insurance requirements, and repair expenses can all contribute to higher premiums.

For New York drivers, the decrease may help, but many may still be paying more than drivers in less expensive states.

Learn more about car insurance in New York.

4. Illinois: Average Rates Fell 11%

Illinois also saw an 11% decrease in average premiums year over year.

Rates in Illinois can vary widely depending on whether a driver lives in a dense metro area, suburban community, or rural region. The statewide decrease in Freeway’s data suggests some customers may be benefiting from more competitive pricing, changing carrier mix, or shifting market conditions.

Learn more about car insurance in Illinois.

5. Arizona: Average Rates Fell 10%

Arizona’s average premiums decreased 10% from Q1 2025 to Q1 2026.

Arizona drivers can face costs tied to traffic congestion, vehicle theft, extreme heat, glass damage, and repair expenses. Even so, Freeway’s data shows average premiums moved lower year over year for single-policy, single-driver auto insurance policies.

Learn more about car insurance in Arizona.

6. Alabama: Average Rates Fell 10%

Alabama also saw a 10% decrease in average premiums.

Weather-related claims, rural road risks, and uninsured drivers can all influence insurance costs in Alabama. But compared with Q1 2025, Freeway customers in the state saw average premiums decline.

Learn more about car insurance in Alabama.

7. Wisconsin: Average Rates Fell 9%

Wisconsin saw average premiums decrease 9% year over year.

Winter weather, rural road conditions, and deer collisions can affect premiums in Wisconsin, but lower congestion in many areas may help offset some cost pressure. The decrease suggests Freeway customers in the state saw measurable relief in 2026.

Learn more about car insurance in Wisconsin.

8. Colorado: Average Rates Fell 8%

Colorado’s average premiums decreased 8% from Q1 2025 to Q1 2026.

Colorado drivers may face insurance costs tied to hail, winter weather, traffic growth, vehicle repair costs, and theft trends. The year-over-year decrease suggests some pricing pressure may have eased for Freeway customers in the state.

Learn more about car insurance in Colorado.

9. Georgia: Average Rates Fell 8%

Georgia saw average premiums decrease 8% year over year.

Georgia drivers can face insurance costs tied to heavy traffic, uninsured drivers, weather-related claims, and vehicle repair expenses. Even with those pressures, Freeway’s data shows average premiums moved lower from Q1 2025 to Q1 2026.

Learn more about car insurance in Georgia.

10. Texas: Average Rates Fell 8%

Texas rounded out the top 10, with average premiums decreasing 8% from Q1 2025 to Q1 2026.

Texas drivers can face costs tied to population growth, severe weather, hail, flooding, traffic congestion, and vehicle repair expenses. The decrease suggests some drivers may be seeing relief, even in a state where local insurance costs can vary widely by region.

Learn more about car insurance in Texas.

States With the Lowest Average Monthly Premiums in 2026

While auto insurance rates vary by state, some markets continue to offer relatively affordable premiums. Freeway’s 2026 analysis found that Idaho, Alabama, New Mexico, Indiana, and Kansas had some of the lowest average monthly auto insurance premiums among the states analyzed, making them some of the most affordable places for drivers to purchase coverage.

*This chart shows the lowest average monthly premiums in Q1 2026 among states included in Freeway’s policy data. Individual premiums may vary based on driver profile, vehicle, coverage level, location, and carrier.

What the Data Does — and Doesn’t — Mean

A statewide average decrease does not guarantee that every driver in that state paid less.

Average premiums can shift based on the mix of drivers, vehicles, coverage levels, carriers, and policy types included in the data. A state’s average may also be influenced by whether more customers purchased minimum coverage, full coverage, higher limits, lower limits, or policies from different carriers.

Still, year-over-year decreases across multiple states are meaningful because they show that premium pressure is not moving in the same direction everywhere. For consumers, that makes comparing rates even more important.

Why Auto Insurance Rates May Be Decreasing in Some States

While every state insurance market is different, several factors can contribute to auto insurance rates stabilizing or decreasing in certain areas. Rate changes are influenced by insurer loss trends, market conditions, regulatory environments, and shifts in consumer behavior.

- Improved insurer profitability: When claim costs stabilize and carriers experience improved loss ratios, insurers may face less pressure to implement additional premium increases or may adjust pricing based on updated market conditions.

- Increased carrier competition: As more carriers write policies in a market, drivers may have access to more options, creating a more competitive pricing environment.

- Lower claim frequency: Fewer accidents, thefts, weather-related losses, or large liability claims can reduce overall claims costs and help ease upward pressure on premiums.

- Changes in customer and policy mix: Average premium trends can shift based on the types of drivers buying policies, the coverage levels selected, vehicle types insured, and other underwriting factors.

- Repair cost stabilization: Vehicle repair costs remain high, especially for newer cars with sensors, cameras, and advanced safety technology. But if repair inflation slows, that may help reduce some pricing pressure.

- Regulatory timing: Insurance rate changes do not always happen immediately. In many states, insurers must file rate changes with regulators, which can delay premium adjustments in response to claim trends.

Even when state averages decline, individual drivers may still see increases. A driver’s rate can change because of accidents, tickets, address changes, vehicle changes, coverage adjustments, lapses in insurance, or carrier-specific pricing decisions.

As market conditions continue to shift, comparing options across multiple insurance carriers can help drivers better understand available coverage choices and find a policy that fits their needs.

What Drivers Can Do If Their Auto Insurance Rates Are Still High

You can’t control statewide insurance trends, but you can take steps to manage your premium and look for savings.

- Shop and compare: Comparing quotes from multiple carriers is one of the most effective ways to look for a better price, especially if your current premium has increased.

- Review your coverage: Make sure your policy still fits your vehicle, budget, and financial risk. Older vehicles may not always need the same level of physical damage coverage.

- Adjust your deductible: Choosing a higher deductible may lower your monthly premium but make sure you can afford the out-of-pocket cost if you file a claim.

- Ask about discounts: Common discounts include multi-car, multi-policy, good student, safe driver, paid-in-full, defensive driving, and paperless billing.

- Consider bundling: Bundling auto insurance with renters, homeowners, or other coverage may help lower overall costs.

- Keep a clean driving record: Accidents, speeding tickets, and other violations can lead to higher premiums.

- Avoid coverage lapses: A lapse in insurance can make it harder or more expensive to get coverage later.

- Think about insurance before buying a vehicle: Some cars cost more to insure because of repair costs, theft risk, safety features, parts availability, or claim history.

Cutting liability limits too aggressively can be risky. After a serious accident, inadequate coverage could leave you responsible for costs your policy does not cover.

How Freeway Insurance Helps Drivers Compare Auto Insurance Rates

Freeway Insurance helps drivers compare auto insurance rates by providing access to options from a wide network of insurance carriers. Instead of a one-size-fits-all approach, Freeway helps customers explore choices and find coverage based on their individual needs, budget, and lifestyle.

Every driver’s journey is different — and their insurance should be too. Whether you’re looking for basic protection, additional coverage, or a new option as your needs change, Freeway makes it easier to compare and choose the coverage that works for you.

Freeway can help drivers shop for:

Freeway gives customers the flexibility to shop their way — online, over the phone, or at a local office. Bilingual English and Spanish-speaking agents are also available in many locations to help customers understand their options and choose the coverage that fits their needs.

Get a fast, free car insurance quote online, call 800-777-5620, or visit one of Freeway’s convenient locations to compare your options.

Methodology

Freeway Insurance analyzed internal policy data for single-policy, single-driver auto insurance policies, comparing Q1 2025 with Q1 2026.

The data methodology reflects actual Freeway Insurance customer policies rather than quote estimates or third-party projections.

State-level averages may be influenced by customer mix, coverage selections, carrier availability, underwriting factors, and regional claims trends.

Frequently Asked Questions

Why did car insurance rates decrease in some states in 2026?

Car insurance rates may decrease when insurance carriers see improvements in claim trends, fewer severe losses, stabilized repair costs, or lower overall expenses. In some states, carriers may adjust pricing as market conditions change, and previous rate increases begin to balance out.

However, rates are personal and can still vary based on factors such as driving history, location, vehicle type, coverage choices, and available insurance options. Comparing rates from multiple carriers can help drivers find coverage that fits their needs and budget.

Which states had the biggest car insurance rate decrease in 2026?

According to Freeway Insurance policy data, Florida had the largest decrease, with average premiums falling 19% from Q1 2025 to Q1 2026. Oregon, New York, Illinois, Arizona, Alabama, Wisconsin, Colorado, Georgia, and Texas also saw notable decreases.

Does a statewide decrease mean my car insurance will go down?

Not necessarily. Statewide averages show broader trends, but your individual rate depends on your personal risk profile, driving history, vehicle, coverage choices, location, and insurer.

Why are auto insurance rates still increasing in some states?

Auto insurance rates may continue to increase in some states due to higher claim costs, severe weather losses, vehicle theft, medical expenses, or other factors impacting the insurance market. Rate changes can also happen at different times by state because insurance companies must follow each state’s approval process before adjusting prices.

How can I find cheaper car insurance?

The best way to look for cheaper car insurance is to compare quotes from multiple carriers. You can also review your coverage, ask about discounts, consider bundling policies, adjust your deductible, and avoid lapses in coverage.

How often should I compare car insurance quotes?

It is a good idea to compare car insurance quotes at least once a year, or anytime your rate increases; you move, buy a new car, add a driver, get married, or experience a major life change.